The Level Isn’t the Story Anymore

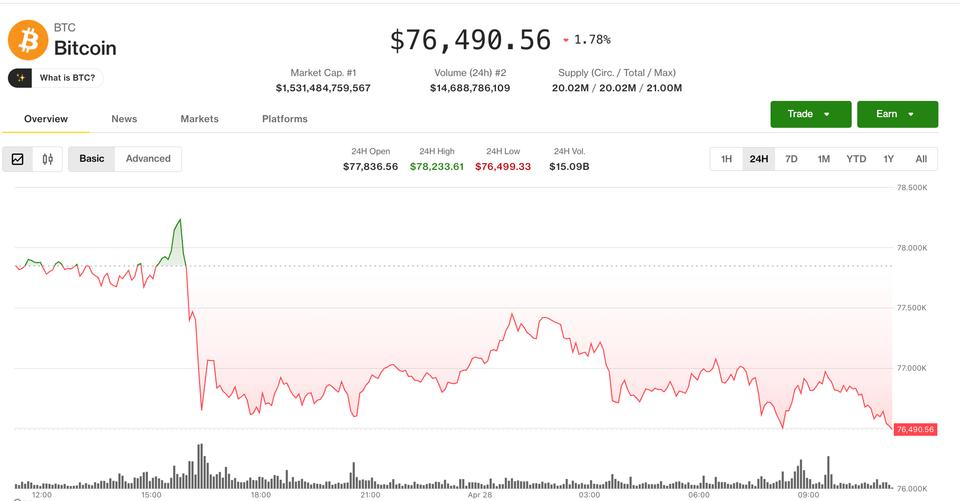

Bitcoin failed at $80,000 for the second time in a week. That part is no longer news — we already wrote about the first attempt. What changed on Tuesday is which indicator finally confirmed it: the Coinbase Premium index flipped negative.

If you trade this market through the lens of where marginal demand is coming from, that single flip is more useful than the price chart. The Coinbase Premium measures the spread between BTC’s price on Coinbase (a U.S.-dominant venue) and on global venues like Binance. Positive readings mean U.S. flow is paying up to get filled. Negative readings mean U.S. flow has stopped being the bid. For most of the rally from $70,000 to $79,500 last week, the premium held positive. Tuesday it didn’t.

This is the cleanest answer to the question we left open four days ago: was this a real institutional bid, or a narrow rally that needed a continuation buyer to show up? The premium tells you the continuation buyer didn’t.

What Derivatives Just Confirmed

The spot signal isn’t alone. Crypto futures open interest dropped over 1% in 24 hours to $120 billion, alongside a 3% volume decline and an 8% drop in liquidations. Cooling activity by every measure that matters.

A few specific reads worth your attention:

- BTC options-to-futures OI ratio fell to 57.5%, the lowest since January 31. That’s a tell that capital is shifting back toward directional futures bets and out of options hedges — historically a precursor to higher short-term realized volatility, not lower.

- BTC futures OI fell to 723.54k contracts, down over 9% from the recent 796.71k high. Position unwind, not new positioning.

- Negative funding rates persist, but the source has shifted. CoinDesk’s read: this leg of negativity is institutional hedging, not outright bearish bets. That’s a different animal — it means the tape isn’t crowded short, but it isn’t crowded long either.

- Implied volatility on both BTC and ETH is sitting at three-month lows. Deribit’s framing was on point: “Negotiation game theory in the Middle East has drugged the BTC Spot market into a deep slumber.” When IV is at lows and spot is range-bound at a clear cap, options structures get cheap to put on.

On Deribit specifically, risk reversals show puts trading at a premium in both BTC and ETH, with BTC puts notably more expensive than ETH puts. That’s the options market voting on which asset has more downside risk into the rest of the week — and it’s voting bitcoin.

The $80,000 Strike Is the Magnet

Here’s the part most readers will miss in the daily noise: the $80,000 strike has been the most actively traded BTC option in the past 24 hours, both in volume and open interest. Block flows featured risk reversals and put spreads on BTC, with put spreads and straddles on ether.

What that translates to: dealer positioning is concentrated exactly where price keeps failing. That’s not coincidence. When dealers are short gamma at the strike where spot keeps tagging, every approach to that level produces the same outcome — sellers showing up, IV staying suppressed, and the rejection being mechanical rather than narrative-driven. Until that strike’s open interest unwinds or rolls higher, $80,000 isn’t a price level. It’s a structural cap.

The Altcoin Tape Is Telling You the Same Thing

The CoinDesk Memecoin Select Index dropped 1.6%, the DeFi Select Index fell 1.2%, and the broader CoinDesk 20 lost 0.8%. Bitcoin-dominant baskets fell less than memecoin baskets — which is the opposite of what a healthy risk-on tape produces.

The exception that proves the rule: apecoin (APE) ripped 17% as traders forced liquidations on a negative long/short ratio, taking out roughly $1 million in shorts. That’s textbook squeeze mechanics in an otherwise sideways tape — isolated, idiosyncratic, not broadening. CoinMarketCap’s Altcoin Season indicator confirms it sits at 39/100, firmly neutral.

DOGE’s OI deserves a separate mention. It climbed 6% in 24 hours to 14.39 billion tokens, the highest since October 10. Positive funding and a rising 24-hour cumulative volume delta show traders are positioning for upside in DOGE specifically — which is what speculative capital does when bitcoin’s range gets boring.

What This Means for Your Trading

Putting the pieces together gives you a usable framework, not just a market recap:

- The trade isn’t long BTC at $77,000 hoping for $80,000 again. It’s positioning around the $80,000 cap until it breaks structurally. A short-dated bear call spread at $80,000 funded by selling premium under $76,000 is a more honest expression of “the cap holds, but I don’t want to be naked short the asset.”

- Watch the Coinbase Premium daily, not weekly. This indicator tends to flip before price confirms direction — it’s the U.S. retail/RIA bid showing up or stepping away. A flip back to positive while spot is still in the $76K–$78K zone is the early signal that another $80K attempt has fuel. A persistently negative premium means the next leg is more likely lower, not higher.

- BTC put premiums above ETH put premiums = relative pair trade. The options market is pricing more downside risk into BTC than ETH this week. If you trust that signal, the cleaner expression isn’t outright BTC short — it’s long ETH against short BTC into Friday.

- Brent above $105 is a hard cap on broader risk. Until U.S.–Iran talks unstall, Brent is doing the work of suppressing IV across crypto. If crude breaks $100 lower on a credible de-escalation headline, that’s where the next $80K attempt actually has structural support, because the IV regime would shift with it.

The Compact Read

The first rejection at $80,000 was the price action. The second rejection is the confirmation. The Coinbase Premium flipping negative is the explanation — U.S. demand stopped paying up, derivatives cooled in unison, and dealer positioning at the $80K strike turned the level into a structural cap rather than a tag-and-go.

This isn’t a bearish thesis. It’s a range thesis. The tape needs something — a Coinbase Premium re-flip, a Brent unwind, a clean break of $76K, or unwind of the $80K strike — to leave the current zone. Until one of those shows up, $77K–$79K is the box, and the trade is structures, not direction.